Why Not to Worry about Core Inflation

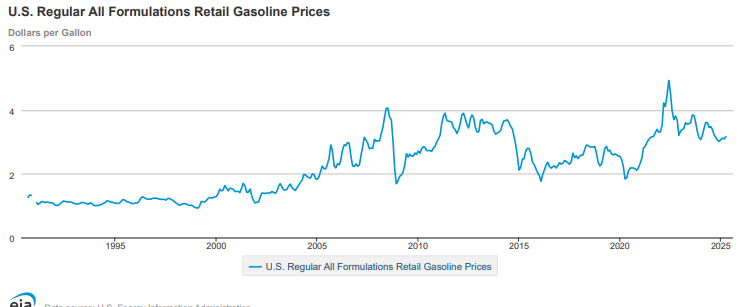

When looking at inflation, you actually have two major divisions: core inflation and food/energy. Food and energy are pulled out because they are very volitile and can swing majorly. For example, look at the average gas price:

You'll find that prices in 2025 are actually lower than back in 2008 and much of the early 2010's. Food is similar. I remember back in college, my wife and I, still dating, would spend typically $35 going out to eat around 1995. Yes, we had some drinks, too. When the boy came along, we cut off the drinks. Through his whole childhood until he launched, we continued under $40 for all three of us. Now that we have AARP cards and he is launched and - you guessed it - eating out is still typically less than $40. In fact, the government makes it a priority to keep food and energy in check - that's because it sets the poverty line for the most part.

Core inflation, on the other hand, is what gets folks really riled up. Anything made of plastic, metal, lumber, concrete, or circuits goes up 2-5% a year. However, there is a silver lining to core inflation. Once you fully own all your stuff, that's what makes one's house value go up. You are getting great asset appreciation for as long as you are able bodied to care for it. If you no longer are, you have a huge chunk of change to cover assisted living - eliminating burden on you children and not having to touch your growing nestegg in your twilight. Your legacy stays intact.

I2Guru uses a flat 3% for its retirement planning inflation rate, but this is actually very conservative compared what one's expenses truly do in retirement. That's because food and energy are the biggest things consumed next to medical - which eventually will be capped with Medicare. Car insurance, you can save by having liability only and if one of you isn't driving anymore anyway, just go to one vehicle and you most likely will be lower than you were 25 years ago overall in retirement. Last, the secondary market is full of great tools and products typically at 30% their new value.

To offset that 3%, you need to think what drives inflation. Target your investments to those sectors and their dividend growth (which should be a major contributor for income investing in retirement) will give you a raise every year! Most dividend paying companies DRIVE INFLATION and the dividend payout goes right along with it.

In sum, don't sweat inflation, just plan for around 3% and recognize the good it is doing for your net worth from your home value and dividend growth.